Baby Food Packaging Market Analysis and Global Forecast 2023-2033

Price range: $ 1,390.00 through $ 5,520.00

Baby Food Packaging Market Research Report: Information By Material (Polymer, Paper, Metal, Glass, Others), By Application (Liquid Milk, Dried Baby food, Powder Milk, Others), and by Region — Forecast till 2033

Baby Food Packaging Market Overview

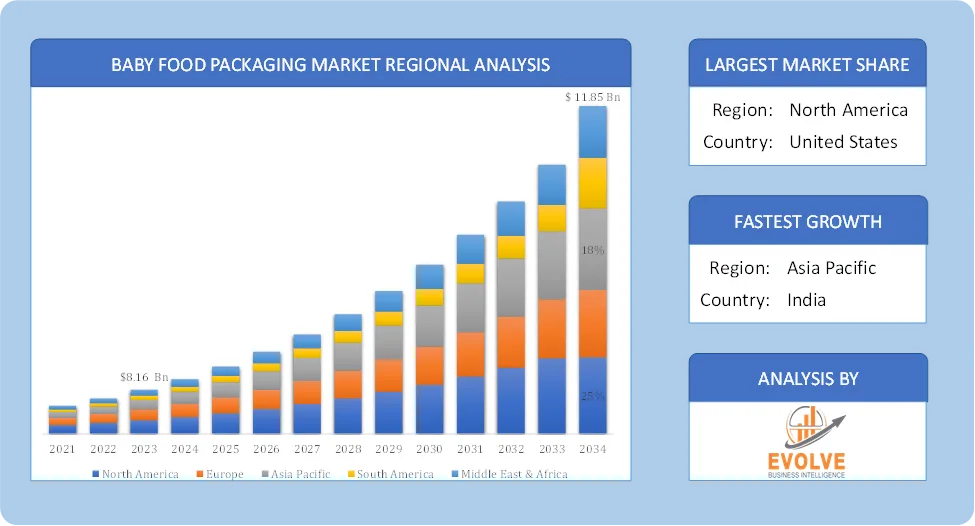

The Baby Food Packaging Market size accounted for USD 8.16 Billion in 2023 and is estimated to account for 9.66 Billion in 2024. The Market is expected to reach USD 11.85 Billion by 2034 growing at a compound annual growth rate (CAGR) of 6.88% from 2024 to 2034. The Baby Food Packaging Market focuses on the development and production of packaging solutions designed to ensure the safety, convenience, and longevity of baby food products. This market is driven by the increasing demand for ready-to-eat baby food, organic baby food products, and sustainable packaging solutions. Increased awareness of the importance of proper nutrition for infant development is driving demand for high-quality baby food and packaging.

The baby food packaging market is evolving to meet the demands of modern parents who prioritize safety, convenience, and sustainability. The demand for BPA-free, eco-friendly, and recyclable packaging has increased due to health-conscious consumers.

Global Baby Food Packaging Market Synopsis

Baby Food Packaging Market Dynamics

Baby Food Packaging Market Dynamics

The major factors that have impacted the growth of Baby Food Packaging Market are as follows:

Drivers:

Ø Growing Demand for Convenience & Ready-to-Eat Baby Food

Increasing number of working parents is driving demand for ready-to-eat and easy-to-use baby food packaging. Portable, lightweight, and resealable packaging formats (pouches, squeeze tubes) are gaining popularity. Strict food safety regulations are pushing manufacturers toward BPA-free plastics, glass, and metal packaging. Growing focus on child-safe, leak-proof, and contamination-resistant packaging solutions. Use of QR codes, NFC tags, and augmented reality (AR) for tracking ingredients and verifying authenticity and extends shelf life by controlling oxygen and moisture levels.

Restraint:

- High Cost of Sustainable & Premium Packaging

Eco-friendly materials (biodegradable plastics, glass, metal) are more expensive than traditional plastic packaging. Costs associated with recyclable and reusable packaging development can affect profit margins. Higher logistics and transportation costs due to the weight of premium packaging (e.g., glass jars). Governments and consumers are pushing for plastic-free and biodegradable packaging, limiting the use of traditional materials. Challenges in establishing large-scale recycling infrastructure in emerging markets slow down sustainable packaging adoption.

Opportunity:

⮚ Rising Popularity of Smart & Intelligent Packaging

Adoption of QR codes, NFC tags, and RFID for product authenticity verification, traceability, and customer engagement. Use of Modified Atmosphere Packaging (MAP) and vacuum-sealed solutions to increase shelf life without preservatives. Growing interest in temperature-sensitive packaging that alerts consumers about storage conditions. The shift toward organic, non-GMO, and preservative-free baby food is driving demand for high-quality, specialized packaging. Luxury baby food brands are focusing on premium glass jars, metal cans, and resealable pouches for better product appeal. Opportunity to introduce customized, limited-edition, and aesthetically appealing packaging designs.

Baby Food Packaging Market Segment Overview

By Material

By Material

Based on material, the market is segmented based on Polymer, Paper, Metal, Glass, Others. The Polymer segment in the Baby Food Packaging market is poised for substantial growth throughout the forecast period, driven by its inherent versatility and adaptability to innovative packaging designs. Polymer materials, including polyethylene, polypropylene, and polyethylene terephthalate, offer lightweight, durable, and cost-effective solutions, aligning with the industry’s emphasis on convenience and sustainability. This segment’s growth is further fueled by the continuous development of advanced polymer technologies, enabling the creation of safe and secure packaging solutions that cater to the evolving demands of parents for efficient and eco-friendly baby food packaging.

By Application

Based on Application, the market segment has been divided into the Liquid Milk, Dried Baby food, Powder Milk and Others. The Liquid Milk segment in the Baby Food Packaging market is poised for substantial growth during the forecast period, attributed to increasing consumer preferences for convenient and on-the-go baby feeding solutions. As demand rises for ready-to-use liquid milk products, the packaging industry is innovating with user-friendly, sterile, and portion-controlled packaging designs, driving the popularity of this segment among parents seeking convenient and nutritionally sound options for their infants.

Global Baby Food Packaging Market Regional Analysis

Based on region, the global Baby Food Packaging Market has been divided into North America, Europe, Asia-Pacific, the Middle East & Africa, and Latin America. North America is projected to dominate the use of the Baby Food Packaging Market followed by the Asia-Pacific and Europe regions.

North America Global Baby Food Packaging Market

North America holds a dominant position in the Baby Food Packaging Market. It’s driven by busy lifestyles and a high demand for convenient packaging solutions. There’s a strong emphasis on product innovation, safety, and extending shelf life and consumers are increasingly seeking organic and premium baby food products, influencing packaging trends. There is also a strong push for sustainable packaging.

Asia-Pacific Global Baby Food Packaging Market

The Asia-Pacific region has indeed emerged as the fastest-growing market for the Baby Food Packaging Market industry. Asia-Pacific region is experiencing rapid growth due to rising disposable incomes, increasing birth rates, and urbanization. E-commerce plays a significant role in expanding market reach. There’s a growing demand for packaged baby food as a convenient alternative to homemade meals. China and India are key markets within this region.

Competitive Landscape

The global Baby Food Packaging Market is highly competitive, with numerous players offering a wide range of software solutions. The competitive landscape is characterized by the presence of established companies, as well as emerging startups and niche players. To increase their market position and attract a wide consumer base, the businesses are employing various strategies, such as product launches, and strategic alliances.

Prominent Players:

- Winpak Ltd

- Bericap India Pvt Ltd

- Bemis Company Inc

- Mondi Group

- Amcor Ltd

- Tata Tinplate Company of India (TCIL)

- Rexam PLC

- Cascades Inc

- Hindustan National Glass & Industries Ltd

- Ardagh Group

- RPC Group.

Scope of the Report

Global Baby Food Packaging Market, by Material

- Polymer

- Paper

- Metal

- Glass

- Others

Global Baby Food Packaging Market, by Application

- Liquid Milk

- Dried Baby food

- Powder Milk

- Others

Global Baby Food Packaging Market, by Region

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Benelux

- Nordic

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- Indonesia

- Austalia

- Malaysia

- India

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of SouthAmerica

- Middle East &Africa

- Saudi Arabia

- UAE

- Egypt

- SouthAfrica

- Rest of Middle East & Africa

| Parameters | Indicators |

|---|---|

| Market Size | 2033: USD 32.88 Billion |

| CAGR (2023-2033) | 10.96% |

| Base year | 2022 |

| Forecast Period | 2023-2033 |

| Historical Data | 2021 (2017 to 2020 On Demand) |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Trends |

| Key Segmentations | Material, Application |

| Geographies Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

| Key Vendors | Winpak Ltd, Bericap India Pvt Ltd, Bemis Company Inc, Mondi Group, Amcor Ltd, Tata Tinplate Company of India (TCIL), Rexam PLC, Cascades Inc, Hindustan National Glass & Industries Ltd, Ardagh Group and RPC Group. |

| Key Market Opportunities | · Rising Popularity of Smart & Intelligent Packaging · Growth of Organic & Premium Baby Food |

| Key Market Drivers | · Growing Demand for Convenience & Ready-to-Eat Baby Food · Rising Health & Safety Concerns |

REPORT CONTENT BRIEF:

- High-level analysis of the current and future Baby Food Packaging Market trends and opportunities

- Detailed analysis of current market drivers, restraining factors, and opportunities in the future

- Baby Food Packaging Market historical market size for the year 2021, and forecast from 2023 to 2033

- Baby Food Packaging Market share analysis at each product level

- Competitor analysis with detailed insight into its product segment, Government & Defense strength, and strategies adopted.

- Identifies key strategies adopted including product launches and developments, mergers and acquisitions, joint ventures, collaborations, and partnerships as well as funding taken and investment done, among others.

- To identify and understand the various factors involved in the global Baby Food Packaging Market affected by the pandemic

- To provide a detailed insight into the major companies operating in the market. The profiling will include the Government & Defense health of the company’s past 2-3 years with segmental and regional revenue breakup, product offering, recent developments, SWOT analysis, and key strategies.

Frequently Asked Questions (FAQ)

What is the growth rate of the global Baby Food Packaging Market?

The global Baby Food Packaging Market is growing at a CAGR of 10.96% over the next 10 years

Which region has the highest growth rate in the market of Baby Food Packaging Market?

Asia Pacific is expected to register the highest CAGR during 2023-2033

Which region has the largest share of the global Baby Food Packaging Market?

North America holds the largest share in 2022

Who are the key players in the global Baby Food Packaging Market?

Winpak Ltd, Bericap India Pvt Ltd, Bemis Company Inc, Mondi Group, Amcor Ltd, Tata Tinplate Company of India (TCIL), Rexam PLC, Cascades Inc, Hindustan National Glass & Industries Ltd, Ardagh Group and RPC Group. are the major companies operating in the market.

Do you offer Post Sale Support?

Yes, we offer 16 hours of analyst support to solve the queries

Do you sell particular sections of a report?

Yes, we provide regional as well as country-level reports. Other than this we also provide a sectional report. Please get in contact with our sales representatives.

Press Release

Global Pharmaceutical Manufacturing Market to Reach $1.38 Trillion by 2035 with 7.35% CAGR, New Research Shows

The Global Mammography Market Is Estimated To Record a CAGR of Around 10.29% During The Forecast Period

Glue Stick Market to Reach USD 2.35 Billion by 2034

Podiatry Service Market to Reach USD 11.88 Billion by 2034

Microfluidics Technology Market to Reach USD 32.58 Billion by 2034

Ferric Chloride Market to Reach USD 10.65 Billion by 2034

Family Practice EMR Software Market to Reach USD 21.52 Billion by 2034

Electric Hairbrush Market to Reach USD 15.95 Billion by 2034

Daily Bamboo Products Market to Reach USD 143.52 Billion by 2034

Cross-border E-commerce Logistics Market to Reach USD 112.65 Billion by 2034

Table of Content

Chapter 1. Executive Summary Chapter 2. Scope Of The Study 2.1. Market Definition 2.2. Scope Of The Study 2.2.1. Objectives of Report 2.2.2. Limitations 2.3. Market Structure Chapter 3. Evolve BI Methodology Chapter 4. Market Insights and Trends 4.1. Supply/ Value Chain Analysis 4.1.1. Raw End Users Providers 4.1.2. Manufacturing Process 4.1.3. Distributors/Retailers 4.1.4. End-Use Industry 4.2. Porter’s Five Forces Analysis 4.2.1. Threat Of New Entrants 4.2.2. Bargaining Power Of Buyers 4.2.3. Bargaining Power Of Suppliers 4.2.4. Threat Of Substitutes 4.2.5. Industry Rivalry 4.3. Impact Of COVID-19 on the Baby Food Packaging Market 4.3.1. Impact on Market Size 4.3.2. End-Use Industry Trend, Preferences, and Budget Impact 4.3.3. Regulatory Framework/Government Policies 4.3.4. Key Players' Strategy to Tackle Negative Impact 4.3.5. Opportunity Window 4.4. Technology Overview 12.28. Macro factor 4.6. Micro Factor 4.7. Demand Supply Gap Analysis of the Baby Food Packaging Market 4.8. Import Analysis of the Baby Food Packaging Market 4.9. Export Analysis of the Baby Food Packaging Market Chapter 5. Market Dynamics 5.1. Introduction 5.2. DROC Analysis 5.2.1. Drivers 5.2.2. Restraints 5.2.3. Opportunities 5.2.4. Challenges 5.3. Patent Analysis 5.4. Industry Roadmap 5.5. Parent/Peer Market Analysis Chapter 6. Global Baby Food Packaging Market, By Material 6.1. Introduction 6.2. Metal 6.3. Glass 6.4. Polymer 6.5. Paper 6.6. Others Chapter 7. Global Baby Food Packaging Market, By Application 7.1. Introduction 7.2. Liquid Milk 7.3. Dried Baby food 7.4. Powder Milk 7.5. Others Chapter 8. Global Baby Food Packaging Market, By Region 8.1. Introduction 8.2. North America 8.2.1. Introduction 8.2.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.2.3. Market Size and Forecast, By Country, 2024-2034 8.2.4. Market Size and Forecast, By Product Type, 2024-2034 8.2.5. Market Size and Forecast, By End User, 2024-2034 8.2.6. US 8.2.6.1. Introduction 8.2.6.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.2.6.3. Market Size and Forecast, By Product Type, 2024-2034 8.2.6.4. Market Size and Forecast, By End User, 2024-2034 8.2.7. Canada 8.2.7.1. Introduction 8.2.7.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.2.7.4. Market Size and Forecast, By Product Type, 2024-2034 8.2.7.5. Market Size and Forecast, By End User, 2024-2034 8.3. Europe 8.3.1. Introduction 8.3.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.3.3. Market Size and Forecast, By Country, 2024-2034 8.3.4. Market Size and Forecast, By Product Type, 2024-2034 8.3.5. Market Size and Forecast, By End User, 2024-2034 8.3.6. Germany 8.3.6.1. Introduction 8.3.6.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.3.6.3. Market Size and Forecast, By Product Type, 2024-2034 8.3.6.4. Market Size and Forecast, By End User, 2024-2034 8.3.7. France 8.3.7.1. Introduction 8.3.7.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.3.7.3. Market Size and Forecast, By Product Type, 2024-2034 8.3.7.4. Market Size and Forecast, By End User, 2024-2034 8.3.8. UK 8.3.8.1. Introduction 8.3.8.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.3.8.3. Market Size and Forecast, By Product Type, 2024-2034 8.3.8.4. Market Size and Forecast, By End User, 2024-2034 8.3.9. Italy 8.3.9.1. Introduction 8.3.9.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.3.9.3. Market Size and Forecast, By Product Type, 2024-2034 8.3.9.4. Market Size and Forecast, By End User, 2024-2034 8.3.11. Rest Of Europe 8.3.11.1. Introduction 8.3.11.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.3.11.3. Market Size and Forecast, By Product Type, 2024-2034 8.3.11.4. Market Size and Forecast, By End User, 2024-2034 8.4. Asia-Pacific 8.4.1. Introduction 8.4.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.4.3. Market Size and Forecast, By Country, 2024-2034 8.4.4. Market Size and Forecast, By Product Type, 2024-2034 8.12.28. Market Size and Forecast, By End User, 2024-2034 8.4.6. China 8.4.6.1. Introduction 8.4.6.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.4.6.3. Market Size and Forecast, By Product Type, 2024-2034 8.4.6.4. Market Size and Forecast, By End User, 2024-2034 8.4.7. India 8.4.7.1. Introduction 8.4.7.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.4.7.3. Market Size and Forecast, By Product Type, 2024-2034 8.4.7.4. Market Size and Forecast, By End User, 2024-2034 8.4.8. Japan 8.4.8.1. Introduction 8.4.8.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.4.8.3. Market Size and Forecast, By Product Type, 2024-2034 8.4.8.4. Market Size and Forecast, By End User, 2024-2034 8.4.9. South Korea 8.4.9.1. Introduction 8.4.9.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.4.9.3. Market Size and Forecast, By Product Type, 2024-2034 8.4.9.4. Market Size and Forecast, By End User, 2024-2034 8.4.10. Rest Of Asia-Pacific 8.4.10.1. Introduction 8.4.10.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.4.10.3. Market Size and Forecast, By Product Type, 2024-2034 8.4.10.4. Market Size and Forecast, By End User, 2024-2034 8.5. Rest Of The World (RoW) 8.5.1. Introduction 8.5.2. Driving Factors, Opportunity Analyzed, and Key Trends 8.5.3. Market Size and Forecast, By Product Type, 2024-2034 8.5.4. Market Size and Forecast, By End User, 2024-2034 Chapter 9. Company Landscape 9.1. Introduction 9.2. Vendor Share Analysis 9.3. Key Development Analysis 9.4. Competitor Dashboard Chapter 10. Company Profiles 10.1. Winpak Ltd 10.1.1. Business Overview 10.1.2. Government & Defense Analysis 10.1.2.1. Government & Defense – Existing/Funding 10.1.3. Product Portfolio 10.1.4. Recent Development and Strategies Adopted 10.1.5. SWOT Analysis 10.2. Bericap India Pvt Ltd 10.2.1. Business Overview 10.2.2. Government & Defense Analysis 10.2.2.1. Government & Defense – Existing/Funding 10.2.3. Product Portfolio 10.2.4. Recent Development and Strategies Adopted 10.2.5. SWOT Analysis 10.3. Bemis Company Inc 10.3.1. Business Overview 10.3.2. Government & Defense Analysis 10.3.2.1. Government & Defense – Existing/Funding 10.3.3. Product Portfolio 10.3.4. Recent Development and Strategies Adopted 10.3.5. SWOT Analysis 10.4. Mondi Group 10.4.1. Business Overview 10.4.2. Government & Defense Analysis 10.4.2.1. Government & Defense – Existing/Funding 10.4.3. Product Portfolio 10.4.4. Recent Development and Strategies Adopted 10.12.28. SWOT Analysis 10.5. Amcor Ltd 10.5.1. Business Overview 10.5.2. Government & Defense Analysis 10.5.2.1. Government & Defense – Existing/Funding 10.5.3. Product Portfolio 10.5.4. Recent Development and Strategies Adopted 10.5.5. SWOT Analysis 10.6. Tata Tinplate Company of India (TCIL) 10.6.1. Business Overview 10.6.2. Government & Defense Analysis 10.6.2.1. Government & Defense – Existing/Funding 10.6.3. Product Portfolio 10.6.4. Recent Development and Strategies Adopted 10.6.5. SWOT Analysis 10.7. Rexam PLC 10.7.1. Business Overview 10.7.2. Government & Defense Analysis 10.7.2.1. Government & Defense – Existing/Funding 10.7.3. Product Portfolio 10.7.4. Recent Development and Strategies Adopted 10.7.5. SWOT Analysis 10.8 Cascades Inc 10.8.1. Business Overview 10.8.2. Government & Defense Analysis 10.8.2.1. Government & Defense – Existing/Funding 10.8.3. Product Portfolio 10.8.4. Recent Development and Strategies Adopted 10.8.5. SWOT Analysis 10.9 Hindustan National Glass & Industries Ltd 10.9.1. Business Overview 10.9.2. Government & Defense Analysis 10.9.2.1. Government & Defense – Existing/Funding 10.9.3. Product Portfolio 10.9.4. Recent Development and Strategies Adopted 10.9.5. SWOT Analysis 10.10. Ardagh Group and RPC Group. 10.10.1. Business Overview 10.10.2. Government & Defense Analysis 10.9.2.1. Government & Defense – Existing/Funding 10.10.3. Product Portfolio 10.10.4. Recent Development and Strategies Adopted 10.10.5. SWOT Analysis

Connect to Analyst

Research Methodology

Our Most Viewed Report and gain instant expertise

Online Travel Agency (OTA) Market Analysis and Global Forecast 2023-2033