Evolve Business Intelligence has published a research report on the Global Oilwell Spacer Fluid Market, 2024–2034. The global Oilwell Spacer Fluid Market is projected to exhibit a CAGR of around 6.54% during the forecast period of 2024 to 2034.

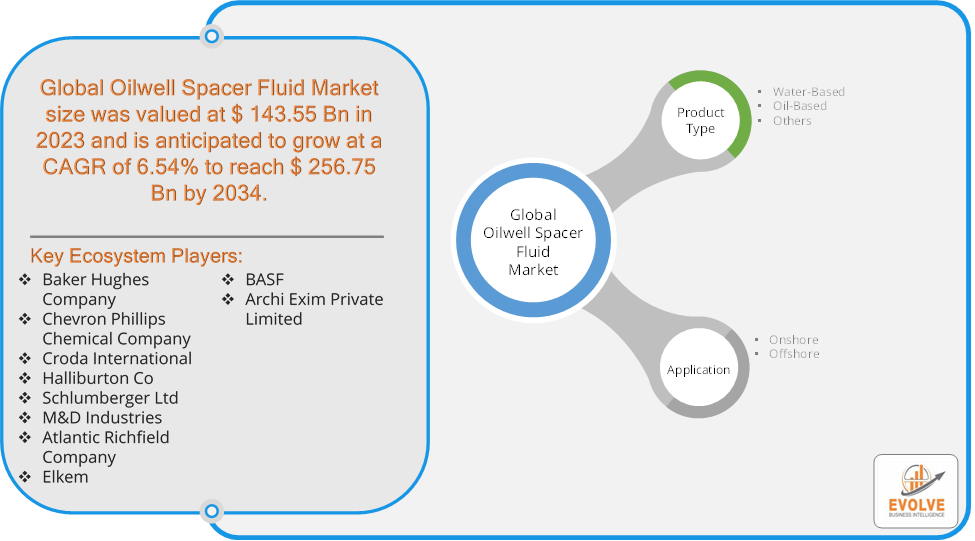

Evolve Business Intelligence has recognized the following companies as the key players in the global Oilwell Spacer Fluid Market: Baker Hughes Company, Chevron Phillips Chemical Company, Croda International, Halliburton Co, Schlumberger Ltd, M&D Industries, Atlantic Richfield Company, Elkem, BASF and Archi Exim Private Limited.

Market Highlights

Market Highlights

The Global Oilwell Spacer Fluid Market is projected to be valued at USD 256.75 Billion by 2034, recording a CAGR of around 6.54% during the forecast period. The Oilwell Spacer Fluid Market refers to the industry that focuses on the production, development, and distribution of spacer fluids used in oil well drilling operations. Spacer fluids are specialized fluids that are pumped between the drilling fluid (also called mud) and the cement slurry during the wellbore completion process. The primary function of spacer fluids is to separate incompatible fluids, such as drilling mud and cement slurry, ensuring efficient displacement of the mud from the wellbore, which is essential for a strong and effective cement bond.

The market’s growth is influenced by fluctuations in oil prices, advancements in drilling technologies, and environmental regulations governing the use of drilling fluids. The oilwell spacer fluid market is a crucial component of the oil and gas industry, ensuring the safe and efficient completion of wellbores.

Segmental Analysis

The global Oilwell Spacer Fluid Market has been segmented based on Product Type and Application.

Based on Product Type, the Oilwell Spacer Fluid Market is segmented into Water-Based, Oil-Based and Others. The Oil-Based segment is anticipated to dominate the market.

Based on Application, the global Oilwell Spacer Fluid Market has been divided into Onshore and Offshore. The Onshore segment is anticipated to dominate the market.

Regional Analysis

The Oilwell Spacer Fluid Market is divided into five regions: North America, Europe, Asia-Pacific, South America, and the Middle East, & Africa. North America, especially the United States and Canada, is a leading market for oilwell spacer fluids due to the significant oil and gas exploration and production activities. The rise of shale gas exploration in the U.S. (particularly in regions like the Permian Basin) and Canada’s oil sands production drive demand for advanced spacer fluids and the region is also at the forefront of technological innovations in drilling techniques, such as horizontal drilling and hydraulic fracturing, which require efficient wellbore cleaning, boosting the demand for high-performance spacer fluids. Europe has significant oil and gas production in countries such as Norway, the UK (North Sea), and Russia. The North Sea remains a key area of offshore drilling activity, particularly for deepwater oil production, where spacer fluids play a critical role in wellbore cleaning and cementing and europe has some of the most stringent environmental regulations for oil and gas exploration. This creates opportunities for spacer fluids that meet high environmental standards and are biodegradable. The Asia-Pacific region, led by countries like China, India, Indonesia, and Australia, is a key growth area for the oilwell spacer fluid market. Rising energy demands, industrialization, and growing exploration activities in onshore and offshore reserves drive the market in this region and the growth in energy consumption and rapid industrialization in countries like China and India present substantial opportunities for the market. Latin America, particularly Brazil, Mexico, and Venezuela, is an important region for oil and gas exploration, especially in offshore drilling activities. Brazil’s offshore pre-salt oil fields and Mexico’s recent energy reforms have led to increased exploration and production, driving demand for spacer fluids. The Middle East is home to some of the largest oil-producing countries in the world, including Saudi Arabia, the UAE, Iraq, and Kuwait. The region’s extensive onshore and offshore oil exploration activities drive the demand for spacer fluids. In Africa, emerging oil and gas markets such as Nigeria, Angola, and Ghana are experiencing growth in offshore exploration, which further boosts market demand.